Rock Health has released its digital health funding figures for the third quarter of 2018, and… they are amazing!

The Q3 2018 was the biggest quarter yet, with $3.3B invested across 93 deals during the period. The record-breaking quarter has also helped push 2018 YTD funding to a total of $6.8B, which is higher than last year’s annual funding!

It was larger deals — rather than number of deals — that helped this bump, with the average deal size on the year soaring to $23.6M. Even excluding the six deals over $200M, average deal size is still greater than last year ($17.6M compared to $16.4M).

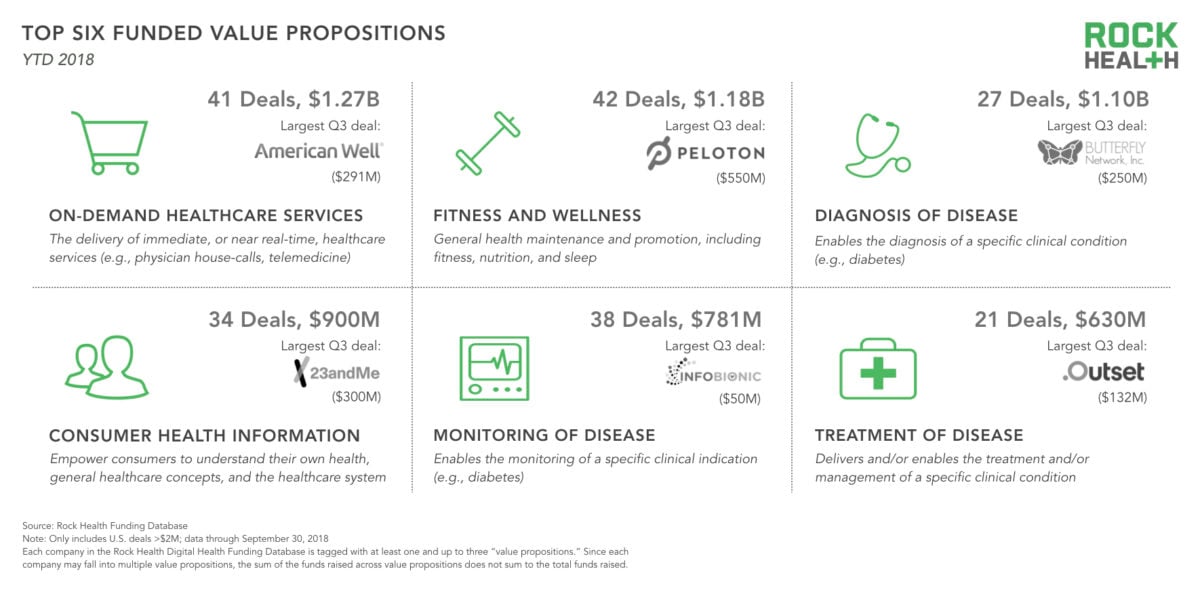

Category-wise, investors poured the most money into companies offering on-demand healthcare services as a primary value proposition — the largest such Q3 round went to American Well ($291M). Other notable categories include digital therapeutics and those companies supporting a shift in the care paradigm.

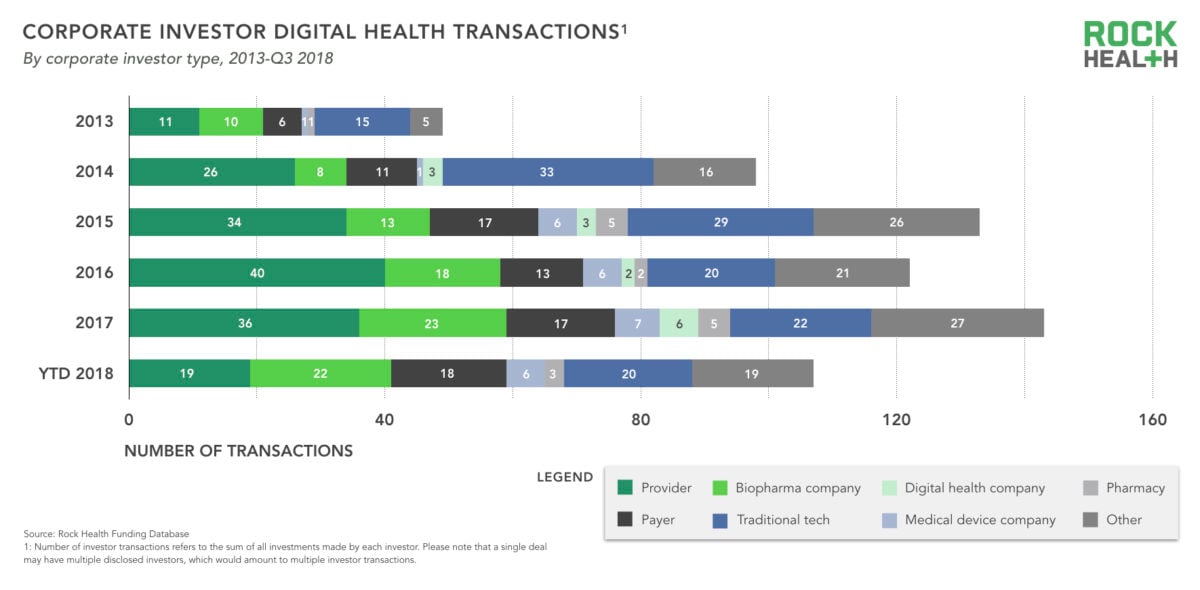

Corporate VCs (CVCs) participated in 15% of investor transactions, and many are investing in digital health companies as part of a broader partnership strategy. Highlights from this and the year before include GSK’s $300M investments in 23andMe, Abbott’s participation in Bigfoot Biomedical’s $55M Series B round, Cigna’s participation in Omada Health’s $50M round in 2017 (expanded their commercial partnership in Q3), and OSF Ventures’ investment in Level Ex.

Overall, corporate VCs completed 102 deal transactions thus far in 2018. Biopharma companies and tech CVCs (e.g., the Amazon Alexa Fund, Baidu Ventures, GV, Comcast Ventures) each accounted for nearly 20% of those transactions. And provider and payer CVCs have each participated in nearly as many deals.

Big tech companies are separately discussed in Rock Health’s report; highlights include Amazon’s acquisition of Pill Pack, Apple’s launch of the Watch Series 4, and Google-owned Nest’s acquisition of smartphone-based health monitoring developer Senosis.

All these efforts represent a mixed signal for smaller companies competing in similar areas: on one hand, some of these startups may now be looking as more attractive acquisition targets; on the other, if they don’t find a bigger partner (acquiror) – they may face an uncertain future fighting with the bigger competitor(s).

Finally, Rock Health discusses exits, which it says remain sluggish, with digital health companies proving to be the most likely acquirer for other digital health startups.

Overall, 82 digital health companies were acquired in the first three quarters of 2018, almost on pace with 2017’s year-end total of 120. Companies focused on enhancing electronic health records and clinical workflow were the most likely to be acquired, with 11 companies making an exit. The IPO drought continues (the last digital health IPO was in 2016), but this isn’t unique to digital health.

Rock Health concludes with a note on market consolidation — adding that it remains to be seen if consolidation in the digital health space will accelerate.